Equity market expectations

What kind of future can broken supply chains, dictatorial Chinese politics, rising inflation, a hawkish Federal Reserve, and a continually fighting Congress bring? The combination sounds like a rough slog for equity market investors – but we believe the opposite. Opportunities arise from challenges, and we see strong prospects ahead.

Supply Chain Disruptions – Inflation, wages, and revenues

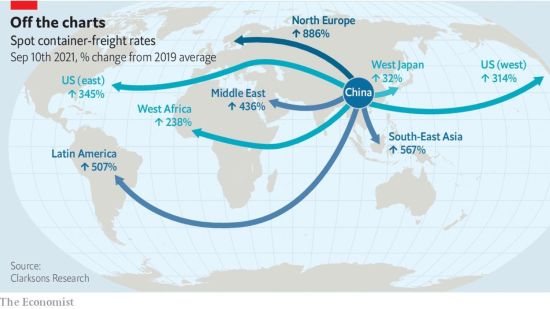

Supply chain disruptions have rattled global trade flows from Shanghai, Dubai, Singapore, and Los Angeles. The result is accelerating price and wage inflation and an inability to source products to meet end demand. Costs to ship a 40-foot container have risen from $4,000 in January to $12,000 last month. Premiums and surcharges are adding another $8,000 to those expenses, all of which consumers are covering.

Port workers are loading and unloading ships around the clock, but their efforts will take several months to return operations to normal. For example, the Port of Los Angeles had 40 ships awaiting unloading in February. By June, the number declined to 10. It quickly increased to 72 before falling to 62 at the end of September.

The upshot is that meeting elevated demand amid higher input costs and general inflation will require specific characteristics from the stocks we own. Companies with proprietary products or services will enjoy and employ pricing power. They also retain the ability to manage costs and maintain production through wage increases, investments in automation, and outsourcing. Possessing these attributes will help produce steady or modestly expanding margins. We have been adjusting our investment strategies to take advantage, selling companies less able to raise prices in favor of those who can.

Chinese Political and Economic Changes

China, the world’s second-largest economy, was the first country to exit the brief 2020 recession. Festering real estate financing issues have become a concern, politically directed regulations are growing, and their military has become increasingly active throughout Asia, specifically in Taiwan and India. While directives and military exercises are not new, they are intensifying the supply chain concerns. Despite some manufacturing moving to Southeast Asia and Latin America, China remains a major global supplier. We expect new regulations to eventually ease and some economic stimulus to counteract a slowing economy following a contraction in factory activity in September, the first time since early 2020.

Our investment strategies are underweight exposure to direct investment in China, which constitutes 10% of the international index and 5% of the world equity index, but many non-Chinese companies source products and sell to Chinese consumers. The recent declines in Chinese stocks and companies with Chinese exposure provide an opportunity to invest in the world’s second-largest and still-growing economy. We are looking for companies with an expanding market, proprietary advantage, and good relations with the Chinese government.

U.S. Government Policy

U.S. policies helped our economy become the locomotive for a global recovery, but it threatens to derail this powerful engine. Investors are concerned with the constant threat of debt ceiling breaches, infrastructure and social spending bills, rising inflation, and upcoming changes to accommodative monetary policy. With the debt ceiling pushed to December 2021, we anticipate an infrastructure bill will be approved, increasing demand for commodities and industrial equipment and the companies that supply them.

Higher inflation and monetary policy moving from an accommodative stance to a neutral stance need not be bad news for stocks; the U.S. stock market has a history of performing well when interest rates rise, so long as they do so slowly. Higher interest rates and improving loan generation will benefit financial institutions as interest income expands from depressed levels.

Unpredictable Labor Markets

With the economy reopening, the U.S. labor markets rebounded more slowly than anticipated. Employment remains 5.3 million jobs below the February 2020 peak despite the U.S. Bureau of Labor Statistic’s estimate of 10.9 million job openings. Labor shortages are affecting multiple industries and regions. More retirements, dual-income households choosing a single income, and prospective employees holding out for higher wages lead to less reliable employment forecasts.

Larger companies such as Wal-Mart and Target increased minimum wages several months ago to attract the best candidates, but smaller competitors cannot always meet the new pay levels. This dynamic will force many small organizations to close while bigger competitors survive the storm and pick up the dislocated business. Larger companies and those investing in automation and outsourcing to increase productivity are investment themes throughout the portfolios.

Despite all these challenges, we look forward to solid earnings reports over the next few quarters, though progress will be made slowly. Solid demand, reorganized and responsive supply chains, creative hiring approaches, and stabilizing margins will be the catalysts driving equity markets higher into 2022.